The Union Budget 2024, presented by Finance Minister Nirmala Sitharaman, introduced several critical amendments to India’s tax framework, aimed at enhancing efficiency, simplifying processes, and resolving long-standing tax issues. These amendments, which will come into force on October 1, 2024, address aspects such as tax dispute resolution, TDS rates, buyback taxation, and compliance for individuals and businesses. Below is an expanded and comprehensive breakdown of these key changes.

1. Vivad Se Vishwas (VSV) Scheme 2.0

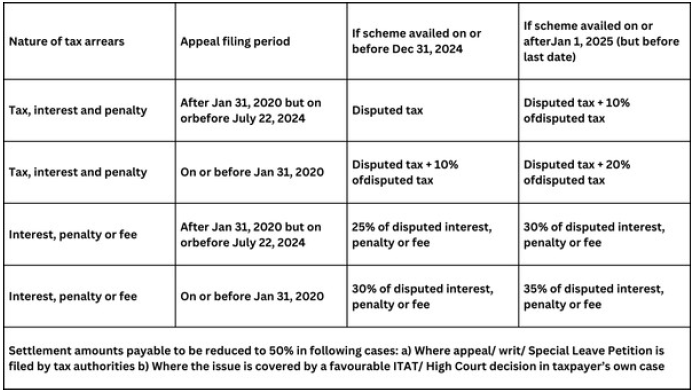

- The original Vivad Se Vishwas scheme, launched in 2020, was successful in resolving a significant portion of tax disputes by offering a simplified settlement mechanism. Based on this success and in response to the continued backlog of pending tax disputes, the government has introduced VSV 2.0.

- Applicability: The new scheme is applicable for cases where disputes related to tax, interest, penalties, or fees are pending as of July 22, 2024, before various appellate authorities, including the High Courts and the Supreme Court.

- Key Benefits:

- Taxpayers can settle disputes by paying a reduced amount, especially in cases where the department has filed an appeal.

- If the tax department initiated the case, the settlement amount can be reduced by 50%, offering taxpayers a more favorable resolution path.

- This version of VSV is focused on reducing the burden on courts and enhancing voluntary compliance.

2. Taxation of Share Buybacks

- Traditionally, companies opted for share buybacks to distribute profits to shareholders while avoiding double taxation (as dividends were taxed but buyback proceeds were not). The new amendments bring buyback taxation in line with dividend taxation.

- New Rules:

- Shareholders will now be liable to pay taxes on buyback proceeds, according to their applicable tax brackets.

- Companies must now withhold TDS (Tax Deducted at Source) at 10% for resident shareholders and 20% for non-residents.

- Capital Loss Treatment: Shareholders can no longer deduct the acquisition cost of shares from the buyback proceeds. Instead, this cost will now be treated as a capital loss, which can be set off against capital gains, if applicable, in future transactions.

- Impact: This will change how companies and investors approach buybacks, potentially reducing the attractiveness of buybacks as a tax-efficient mechanism for returning capital to shareholders.

3. Reduction in TDS Rates for Key Payments

- In an effort to streamline tax collection and reduce the tax burden on individuals, several TDS rates have been revised downward:

- Section 194DA: The TDS on life insurance policy payouts will be reduced from 5% to 2%. This applies when the payout is taxable in the hands of the policyholder.

- Section 194G: The TDS on commissions for the sale of lottery tickets will be reduced from 5% to 2%.

- Section 194H: The TDS on brokerage and commission payments will also be reduced from 5% to 2%.

- Section 194-IB: Individuals and HUFs (Hindu Undivided Families) paying rent will see the TDS reduced from 5% to 2%.

- Section 194M: The TDS on payments made by individuals or HUFs for specific contracts or services (e.g., personal contractors) will drop from 5% to 2%.

- Section 194-O: E-commerce operators will see a major reduction in the TDS rate when paying e-commerce participants, dropping from 1% to 0.1%.

- Impact on Taxpayers: These reductions will ease cash flow issues for taxpayers, especially small businesses, agents, and contractors, by lowering the upfront tax deducted from their earnings.

4. Amendments to Penalty Provisions Under the Black Money Act (BMA)

- The Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, imposes penalties on individuals who have undisclosed foreign assets. However, to address concerns about minor undeclared assets, a key amendment has been introduced:

- New Exemption: If the value of the undisclosed asset does not exceed Rs. 20 lakh, the penalties under Sections 42 and 43 of the BMA Act will not apply.

- Impact: This provides relief to individuals with minor compliance issues, reducing the fear of excessive penalties for small errors.

5. Securities Transaction Tax (STT) Increase for Futures and Options

- To align with the growing trading volume in derivative markets and to ensure that tax collection reflects the actual value of transactions, the government has increased the STT on futures and options (F&O) trading:

- STT on Futures: Increased from 0.0125% to 0.02%.

- STT on Options: Increased from 0.0625% to 0.1% of the premium amount.

- Impact on Investors: Traders and investors in derivative markets will face higher transaction costs, potentially influencing their trading strategies.

6. Discontinuation of Aadhaar Enrolment ID for PAN Applications

- As part of the ongoing efforts to ensure that Aadhaar is used as the primary identification for tax purposes, the provision that allowed individuals to use an Aadhaar Enrolment ID instead of their Aadhaar number in PAN applications and income tax returns will be discontinued from October 1, 2024.

- Impact: Individuals who are yet to obtain their Aadhaar card will need to ensure they have the official number before completing tax filings or applying for PAN cards.

7. TDS on Government Bonds and Floating Rate Savings Bonds

- From October 1, 2024, TDS at 10% will apply to interest income from central and state government bonds, including Floating Rate Savings Bonds.

- TDS Exemption: No TDS will be deducted if the total interest income is less than Rs. 10,000 in a financial year.

- Impact on Investors: This amendment will impact investors holding government bonds, but the Rs. 10,000 exemption provides relief for small investors.

8. Relief on Mutual Fund Repurchase TDS

- In a significant relief to mutual fund investors, the 20% TDS on mutual fund repurchases will be withdrawn.

- Impact: This move is expected to provide relief to mutual fund investors, enhancing the appeal of mutual fund investments, particularly for those engaging in repurchase or redemption of units.

9. Clarification on TDS for Immovable Property Transactions

- Section 194-IA now clarifies that a 1% TDS applies on the sale of immovable property worth more than Rs. 50 lakh, even in cases involving multiple buyers or sellers. The TDS is to be deducted collectively, ensuring compliance in such transactions.

- Impact: Buyers and sellers involved in joint property transactions will need to carefully track the collective value to comply with the TDS requirements.

Conclusion

These detailed amendments reflect the government’s focus on simplifying the tax system, promoting compliance, and addressing longstanding issues in tax policy. The reductions in TDS rates and the introduction of the VSV 2.0 scheme demonstrate the government’s intent to provide relief to taxpayers, while the increased transparency in buyback taxation and securities transaction tax reflects the government’s push for aligning tax policies with modern market practices.

Taxpayers, businesses, and investors are advised to stay informed about these changes, ensure compliance, and adjust their tax planning strategies accordingly to take full advantage of the benefits and avoid any potential penalties.

This expanded version provides deeper insights into each amendment and anticipates the broader impact of these changes on different stakeholders.